Frequently Asked Questions: Opportunity Zones

Get this in PDF form.

Small geographic areas where individuals and corporations can get large capital-gains tax breaks for investing.

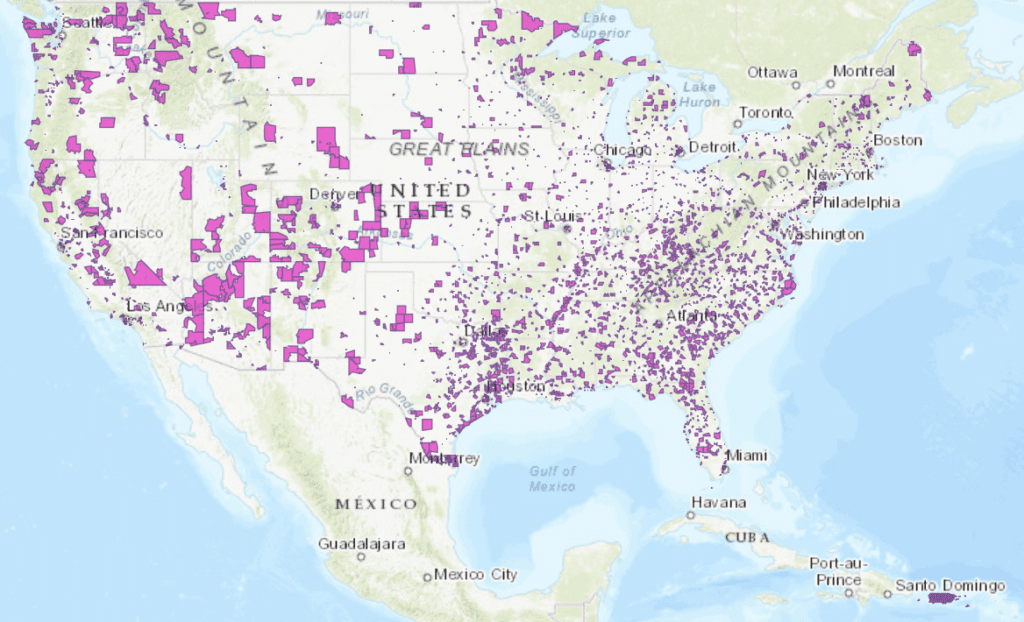

Today, there are 8,764 OZs located in all 50 states, the District of Columbia and five U.S. territories. Nearly all of Puerto Rico is an Opportunity Zone.

- Find out: Where OZs are located where you live.

The goal behind OZs is to stimulate reinvestment in economically depressed areas, and thus, by implication, to help improve the lives of low-income residents in these historically excluded communities. However, on this implied goal of assisting incumbent residents, OZs have no community benefits mechanisms to ensure anything good happens to OZ residents.

- Learn more about Community Benefits Agreements here.

Their arrival was enabled by a provision of the 2017 Tax Cuts and Jobs Act (sometimes referred to as the “Trump Tax Cuts”). But for years before that, a group of tech investors (including Napster’s Sean Parker) had been lobbying for a similar program as a way to avoid or reduce capital gains taxes on their soaring stock portfolios.

Based on 2010 census data, a total of 42,176 census tracts were poor enough to qualify as OZs. The Tax Cuts Act then required each state’s governor to select about one-fourth of the eligible tracts as OZs. The Act also allowed governors to designate better-off census tracts that border OZ-eligible tracts as OZs (for up to 5% of a state’s OZs).

Of the final 8,762 selected, 8,532 were low-income communities and 230 were so-called “contiguous communities” (2.6%).

- Story idea: How were tracts chosen in your state? Are there property owners, developers, mayors, county executives or others who may have influenced the governor’s picks?

By encouraging individuals and corporations to redirect capital gains earnings into OZ projects. These investments can be in real estate (such as office buildings, apartments, or condominiums), or most kinds of individual businesses (such as services, manufacturing, or mining) or other enterprises.

Capital gains is the profit one makes on selling something they own – an asset like a stock or house, for example –that has increased in value over time.

Say you bought shares in a tech stock years ago, and now they are worth $50 million more than when you bought them. The $50 million are unrealized gains. You want to sell but you’ll have to pay $10 million in federal income taxes, or 20% of the gains. (That is already a huge tax break; if your adjusted gross income — of salary, interest, dividends, etc., minus deductions — were $520,000 in 2020, you’d pay 37% federal income tax on that.)

But instead, to avoid the 20% tax, you can sell the shares and invest the $50 million in an OZ. Three generous tax breaks ensue:

The first is that you defer paying that $10 million in capital gains tax. Second, you can hold the investment in the OZ for several years and you’ll get a significant reduction in those taxes when the time comes to pay the original capital gains tax. Third, if your OZ investment appreciates, any additional capital gains you make from the new investment are completely tax-free after 10 years.

- Did you know: Along with OZs, real estate investors enjoy significant and numerous tax breaks.

Rather than investing their capital gains directly in OZ projects, people and corporations put their money in Qualified Opportunity Funds, or QOF. Those financial vehicles pool money from various investors to generate funding for OZ projects. Anyone can create an QOF and they are organized as corporations, partnerships, or a limited liability corporation (LLC) created for the project. Some have a particular region or a state focus, but many invest nationally. Many have minimums, in thousand or even millions, on how much can be invested.

The use of a corporate structure such as an LLC enables QOF investors to hide their identities.

- Story idea: What can or cannot be told about QOFs that have registered with your state’s Secretary of State corporate registration system? How many were created by community based or grassroots organization?

Hard to say. The legislation setting them up doesn’t require public reporting by individuals or corporations in any systematic ways.

But we do know the type of people and companies that are even able to consider OZ investing, and that’s those that have capital gains. In the U.S., 85% of capital gains are generated by just 5% of taxpayers. Most of those are White individuals. One study found that OZ investors have an average household income over $1 million. Also, as mentioned above, many QOF set up minimum amounts that can be invested in them, effectively allowing only the very wealthy to invest.

Yet most OZ incumbent residents are black or Latino and low-income.

- Story idea: Profile current OZ residents and what they would like to see in their community.

Because investors want to maximize their profits, they will seek those OZs most likely to experience rising property values over the next decade. Consequently, high-end real estate development projects in urban gentrifying areas have been popular among investors.

Because the zones were created in 2018, eight years after the 2010 census, it was already evident that some zones were attracting new investments and gentrifying. One real estate advisory firm even issued a public report naming the hottest OZs for investors to choose.

In Houston, a prominent growth expert detailed the risk in his article, “Opportunity Zones: Gentrification on Steroids?”

More than four-fifths of the zones are not getting any investment at all: One study based on tax returns found that only 16% of all OZs received OZ investments; 84% of OZs received none. Additionally, based on news articles, we see that neither Black and Hispanic-owned businesses nor rural areas have been receiving OZ investments.

- Story idea: What’s the median income in the tracts that were chosen compared to ones left out? Any notable ones left out or included?

Unfortunately, no. In addition to what we’ve mentioned about the lack of transparency, the program does not require local hiring, a living wage for construction or service workers, or any affordable, senior or workforce housing units. There are also no requirements for investors to engage with local communities. In other words, there are no safeguards to ensure local residents will benefit in any way from OZ projects.

- Did you know: Our OZ resource page lists many articles about OZ projects, including high-profile ones involving Under Armour billionaire founder Kevin Plank and Cleveland Cavalier billionaire owner Dan Gilbert.

We get that question a lot. Because there are no transparency provisions attached to the program, there is no valid way to evaluate the program. However, a growing body of academic research is showing that the program has not been delivering on its promises. Most projects we know about are real estate, with only a small fraction going to business development.

If by “working,” you mean is the program awarding capital gains tax breaks to wealthy investors, the answer is clearly yes. If you are asking: “Do OZs cause reinvestment in depressed areas that would not have happened otherwise?” there is no valid way to answer that question, especially because some of the chosen census tracts were already gentrifying. Finally, if you are asking: “Are low-income OZ residents benefiting from OZ investments?” there are likely anecdotal examples of that happening. But in the big picture, it would be very hard, if not impossible, to isolate the effect of OZs as a single variable in affecting people’s lives. And any valid cost-benefit analysis would have to weigh other ways in which the same amount of federal dollars could be spent to directly aid working families.

The Joint Committee on Taxation estimated the program will cost the U.S. Treasury about $1.6 billion between 2018 and 2027. However, some argue that the federal cost will likely be higher. As well, these estimates don’t include two other costs that should be considered: 1) state revenue loss and 2) state and local subsidies often given on top of the OZ subsidies. Unfortunately, there are no clear or comprehensive estimates for either one.

OZs have a direct and negative impact on state revenues because most states tie their personal and corporate income tax systems to the federal one. When a state follows federal rules, it is called conformity; when a state chooses to exempt itself from a federal tax rule, that’s known as “decoupling.” To illustrate: when an individual gets a federal OZ tax break on her gains, her Adjusted Gross Income (AGI, or taxable income) is lowered. In most states, she then uses that lower AGI on her state tax return, lowering her state income tax obligation too. Essentially, it’s a form of double dipping.

Georgia estimates it lost $10 million this way in FY 2020, and Oregon estimates it will lose $22.8 million combined from FY2021-2013. Combining those states that had already decoupled from the federal AGI and those that have done so specifically regarding Opportunity Zones, only five states with income taxes have protected themselves from these passive revenue losses.

- Story idea: Has my state decoupled? What are the revenue losses from not decoupling?

Several states enacted additional state-level OZ subsidies to attract investors. For example, Ohio created a state income tax credit that is equal to 10% of an OZ investment in that state. As of 2020, this tax credit has already cost the Buckeye State $26.5 million. Maryland has allowed OZ investors to benefit from larger tax credits under existing tax subsidies. There are also localities that created their own local OZ subsidies. For example, Montgomery County in Maryland has excluded projects in OZs from paying its Development Impact Tax, a special tax that supports local public transportation and schools.

- Story idea: Has your state or community created any add-on subsidies to OZ programs?

Repeal: Some in Congress have proposal repealing the OZ tax break. This would not cancel existing deals, but it would prevent any new QOFs from occurring. Given OZs’ profound flaws and predictable shortfalls, Good Jobs First’s professional opinion favors this option. If asked, we would also recommend that states repeal their add-on OZ subsidies.

Disclosure: Some in Congress, including OZs’ original key sponsor, have proposed amendments to provide more sunshine on QOFs. Their efforts have been unsuccessful. Good Jobs First always favors disclosure, but in this case, we believe that data on OZs would not make a meaningful change in how we understand them; enough is already known.

Decoupling: As explained above, states can protect themselves from passive revenue losses by decoupling from the federal Adjusted Gross Income definition.

Maybe we can answer them. Feel free to email Kasia Tarczynska at [email protected].

Happy digging.

Sources: U.S. Department of Housing and Urban Development, Joint Committee on Taxation, Urban Institute, Center on Budget and Policy Priorities, University of California at Berkeley, NYU Stern School of Business, Georgia Governor’s Office of Planning and Budget, Oregon Department of Revenue, Ohio Development Services Agency, Montgomery County, GeekWire, Forbes.